Global perspective: Do insurance companies fail?

Life insurance is one of the few promises which is designed to outlast generations. For that promise to endure, the financial strength of insurers must be as resilient as the commitments they make. Yet in today’s volatile environment, insurers themselves are vulnerable to the failures.

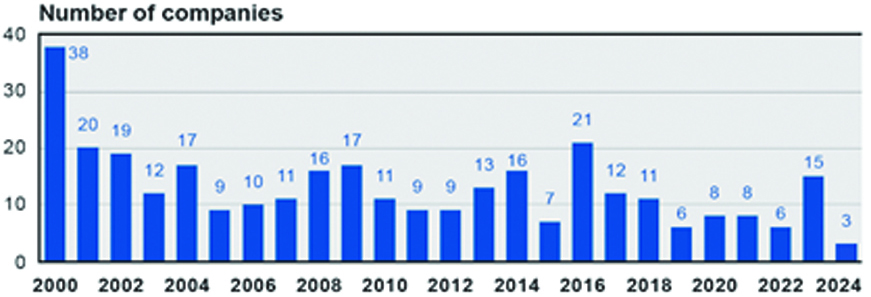

Have life insurance companies actually failed? The answer is “yes”. Over the past 24 years, 324 life insurance companies worldwide have collapsed—an average of 13 each year according to PACICC (Property and Casualty Insurance Compensation Corporation). These failures were not confined to any specific geography or business model; they have been a global reality.

PACICC has identified 324 Life insurers that failed around the globe between 2000 and 2024.An average of 13.0 Life insurers failed each year.

Source: PACICC

The reasons are well known as poor risk selection, mispriced products, inadequate reserving, reinsurance defaults, fraud, and overly complex structures. Historically, such weaknesses eroded the solvency from within. But today, external pressures are just as severe. Climate change has intensified natural catastrophes, increasing both their frequency and severity. What were once local, or cyclical shocks have become systemic threats. The survival of insurers is now inseparable from their ability to withstand nature’s volatility.

This is why regulators worldwide turned to Risk-Based Capital (RBC) framework in the early 1990s. RBC marked a decisive shift from static solvency margins to risk-sensitive capital standards, requiring insurers to hold capital in proportion to their actual exposures of risk. What began in the United States got spread globally including Nepal.

Introduction: A New Era of Insurance Regulation in Nepal

Nepal’s insurance industry has long stood as a guardian of financial security, helping individuals and families to navigate risks and safeguard their futures. But as the sector has grown in terms of size, scope, and complexity, so too has the need for a regulatory framework that keeps pace with the modern challenges. In response to this evolution, the Nepal Insurance Authority (NIA) has taken a historic step forward: the introduction of the Risk-Based Capital (RBC) regime.

This paradigm shift represents not just a change in how capital adequacy is measured, but a complete transformation as to how insurers evaluate, manage, and respond to the risks. By aligning regulatory capital with the true risk profile of each insurer, RBC offers a forward-looking, dynamic framework designed to enhance policyholder protection, market stability, and long-term growth.

This article explores what Risk-Based Capital means, why it matters, how it will reshape the insurance landscape in Nepal, what are the global lessons which can be learnt, and what insurers, regulators, and stakeholders must do to prepare for a successful transition.

Understanding Risk-Based Capital: Moving Beyond One-Size-Fits-All

Risk-Based Capital (RBC) has been one of the most significant regulatory shifts in the insurance sector over the past three decades. At its core, RBC is about aligning an insurer’s capital requirements with the actual risks it carries—whether from underwriting, investments, operations, or external shocks. Moving away from fixed solvency margins toward risk, sensitive capital requirements make capital based on the risks presented by different insurers, who have a choice in dealing with different product designs and managing their risks. RBC helps to protect policyholders by ensuring market stability and prepare the insurers for more volatile future. For Nepal, adopting an RBC framework marks a turning point in the maturity of its insurance market. It positions the country within a broader global movement toward stronger solvency standards and better governance.

Under the Risk-Based Capital framework, capital requirements are calculated based on a comprehensive assessment of risks specific to each insurer. These risks typically fall into the following categories:

- Market Risk: The risk of adverse movements in investment markets impacting the value of assets backing policyholder liabilities.

- Credit Risk: The risk of counterparty default, particularly in reinsurance, investment portfolios, and premium receivables.

- Life Insurance Risk: The risk of claims deviating from expected patterns due to changes in mortality, morbidity, or persistency.

- Operational Risk: The risk arising from internal process failures, system breakdowns, fraud, or human error.

The RBC model assigns capital charges (based on stress scenarios) to each risk category, which are then aggregated (using correlation matrices) to determine the total required capital. An insurer must maintain capital in excess of this threshold to remain solvent. The regulator has prescribed the minimum threshold of 130% as solvency capital in Nepal.

Global Evolution of RBC

The journey of RBC began in the United States in 1993, when the National Association of Insurance Commissioners (NAIC) introduced the first formal RBC system for life insurers. This approach replaced blunt solvency margins with capital charges calibrated to risk categories such as asset quality, underwriting exposures, and interest rate sensitivity.

Europe soon followed its own path, moving from Solvency I to Solvency II in 2016. Solvency II remains the most sophisticated global model, offering both a standard formula and internal models approved by regulators, supported by diversification credits and advanced risk correlation tools.

In Asia, Singapore introduced RBC in 2004, refining it into RBC2 by 2020, which emphasized market-consistent valuation and diversification benefits. China’s C-ROSS (2016) mirrored Solvency II’s three-pillar structure, while Korea’s K-ICS and Japan’s evolving RBC regime show a steady march toward global convergence.

South Africa’s Solvency Assessment and Management (SAM) also stands out as a regional leader, modeled closely on Solvency II.

Why Nepal has adopted RBC: Context and Rationale

Why Nepal has adopted RBC: Context and Rationale

Over the past five years, Nepal’s life insurance sector has steadily expanded its gross written premium (GWP), reflecting both rising awareness and deeper market penetration. In fiscal year 2020-21, life insurers collected around Rs 118 billion as gross written premium (GWP), which grew to Rs 182 billion in the year 2024-25 making an increase of 5 years CAGR of 9%. This trajectory underscores not only stronger demand for financial security but also the impact of regulatory support, Covid-19, digital distribution, and microinsurance reaching underserved areas. While the pace of growth has varied year to year, the overall climb signals a sector that is maturing and broadening its role in Nepalese economy.

Considering the growth in the insurance sector, the adoption of the Risk-based capital becomes even more imperative. The growth in the sector leads to the necessity of various factors as below:

- Market Maturity: As Nepal’s life insurance sector grows—with over NPR 182 billion in annual premiums and millions of active policies—there is a need for more sophisticated risk oversight.

- Diverse Risk Profiles: Insurers vary significantly in product mix, investment strategies, and risk appetite. A flat capital regime ignores this diversity and may lead to regulatory blind spots.

- International Best Practices: RBC aligns Nepal with global standards promoted by the International Association of Insurance Supervisors (IAIS) and is already adopted in neighboring markets such as Sri Lanka, Malaysia, and Thailand.

- Strengthening Policyholder Protection: By ensuring that each insurer holds adequate capital for its unique risks, RBC enhances the sector’s ability to honor claims even during the periods of stresses.

- Reducing Systemic Risk: The framework encourages insurers to monitor and mitigate their exposures proactively, thereby improving the resilience of the entire financial ecosystem.

Key Features of Nepal’s RBC Framework & Comparatives

Nepal’s RBC framework sits closer to Singapore’s RBC2 than Europe’s Solvency II, given its focus on standardized modules and ORSA rather than fully-fledged internal models. Compared to India, which still relies on a solvency margin of 150% but is piloting Ind-RBC through Quantitative Impact Studies (QIS), Nepal is moving faster toward risk sensitivity.

Unlike Solvency II, Nepal’s framework has yet to fully incorporate diversification credits or advanced correlation matrices, but the direction is clear: toward a model-based regime that prioritizes resilience.

Though specific implementation guidelines are still being developed, Nepal’s RBC regime is expected to include the following pillars:

- Quantitative Risk Measurement: Risk-specific capital charges calculated using standardized formulas or internal models.

- Solvency Ratio Benchmark: A new solvency control level (e.g., 130%) above which insurers are deemed financially sound.

- Supervisory Ladder of Intervention: Regulatory responses tiered by the insurer’s solvency ratio (e.g., early warning, intervention, restriction on dividends).

- Disclosure and Transparency: Enhanced reporting of capital adequacy, risk exposures, and stress test results.

This integrated approach seeks to strike a balance between protecting policyholders, encouraging innovation, and fostering market discipline.

Impact of RBC on Life Insurer in Nepal

Nepal’s insurance regulator officially introduced the Risk-Based Capital (RBC) regime through the Risk Based Capital and Solvency Directive, 2022 (2078), aiming to align capital requirements with the real risks insurers face rather than using crude fixed thresholds. Before RBC, Nepal’s fixed-capital regime demanded a flat solvency margin—regardless of business complexity or risk—in effect sheltering capital inefficiencies. The shift to RBC slapped a mirror up to real capital needs.

Look at the jump: under the old regime, the average solvency ratio hovered around 295%, but once RBC’s risk filters were switched on, it slid to roughly 228% in 2023–24. That average fall is more than a statistic—it tells the story of an industry finally rebalanced to its real risk footprint. The key reason for decrease in the solvency margin results is due to higher capital charge on various risk metrics as prescribed by the regulator. Going forward, the RBC more being a global approach shall be adjusted to the local environment which shall further ease the solvency margin of the companies in future to come.

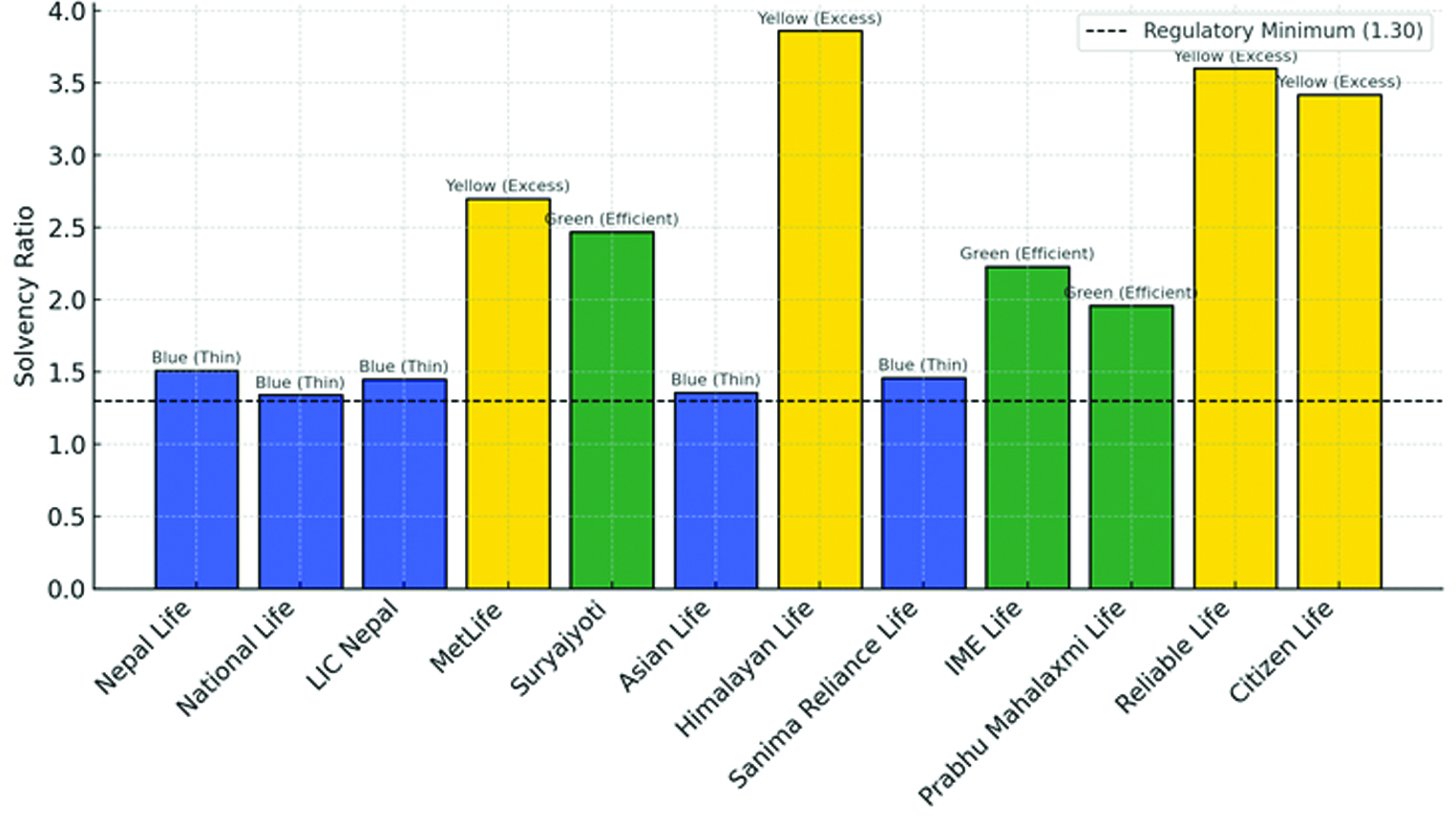

- Fully Efficient Capital (<1.8): Nepal Life, National, LIC Nepal, Asian Life, and Sanima Reliance Life are operating with just enough buffer above the regulatory minimum. Their capital is working hard, but the trade-off is thinner protection against any adversities or shocks.

- Moderate Capital (1.8–2.5): Prabhu Mahalaxmi Life, IME Life, and Surya Jyoti Life sit in the middle ground. They hold a cautious buffer without drifting into excess, balancing safety with efficiency.

- Excess Capital (>2.5): MetLife, Himalayan Life, Reliable Life, and Citizen Life stand out with high ratios. From a policyholder’s view this is reassuring, but from a capital productivity standpoint it points to reserves that may be under-utilized unless linked to growth or dividend plans.

On an average, the industry has shifted from a broad cushion under the fixed regime (≈295%) to a tighter alignment under RBC (≈228%). The new framework exposes some companies to solvency risks and capital inefficiencies to others, showing who is just surviving, who is balanced, and who is sitting on idle capacity.

Implications for Nepal’s Life Insurance Industry

1. Financial Strength and Resilience

RBC will usher in a more stable insurance industry where each company’s capital is better matched to its actual risk profile. Insurers offering high-guarantee products or with concentrated investment portfolios will need to hold more capital, indicating capital commensurate with risk.

2. Strategic Rebalancing of Product Portfolios

Guaranteed-return products and long-term endowments carry higher capital charges due to longer tenure and interest rate risks. This may encourage insurers to change the product mix:

- Term life insurance: This product has a lower interest rate capital burden due to limited duration and lower guarantees, but this will increase mortality risk capital. So, there is a need to create the right mix of portfolios.

- Participating products: Risk-sharing with policyholders.

- Unit-linked insurance plans (ULIPs): Investment risks are borned by the policyholders.

Insurers will need to re-evaluate pricing, profitability, and product mix through a capital-efficiency lens.

3. Investment Discipline and Asset Matching

The new regime will penalize overly risky or illiquid investments with higher capital charges. Insurers will be incentivized to:

- Improve asset-liability matching by optimizing capital requirement.

- Reduce exposure to volatile equity or non-rated instruments.

- Maintain diversified and high-quality investment portfolios.

This will deepen the link between actuarial projections and investment strategy.

4. Competitive Differentiation and Market Consolidation

Larger, well-capitalized insurers with advanced risk management capabilities will gain a competitive edge. Conversely, smaller players with thin capital buffers may:

- Need to raise additional capital.

- Explore mergers or acquisitions.

- Focus on niche products or regional strengths.

Over time, this may lead to a leaner, more efficient insurance landscape with greater customer focus.

5. Rise in Internal Risk Culture and Governance

RBC implementation will force insurers to strengthen internal frameworks, including:

- Enterprise risk management (ERM)

- Actuarial modeling and scenario analysis

- Board-level risk oversight

- Stress testing and ORSA (Own Risk and Solvency Assessment)

This cultural shift will be critical for long-term sustainability and stakeholder confidence.

Global Lessons and Regional Benchmarks

Global Lessons and Regional Benchmarks

Nepal’s Risk-Based Capital framework is borrowed from the international models but is in the tailoring process to its own market maturity and institutional capacity. Unlike Solvency II in Europe or Singapore’s RBC2, Nepal’s approach is starting with standardized modules and stronger supervision rather than complex internal models. This is the right path for now — building foundations in actuarial practice, IT systems, Enterprise Risk Management, and risk culture before layering in sophistication.

Regionally, India is still in transition through QIS studies, Malaysia’s 2009 adoption spurred product innovation, and Thailand phased in reforms to allow insurers time to adapt. The common lesson: go gradual, encourage regulator–industry dialogue, use standard templates, and create safe “sandbox” spaces to test new approaches.

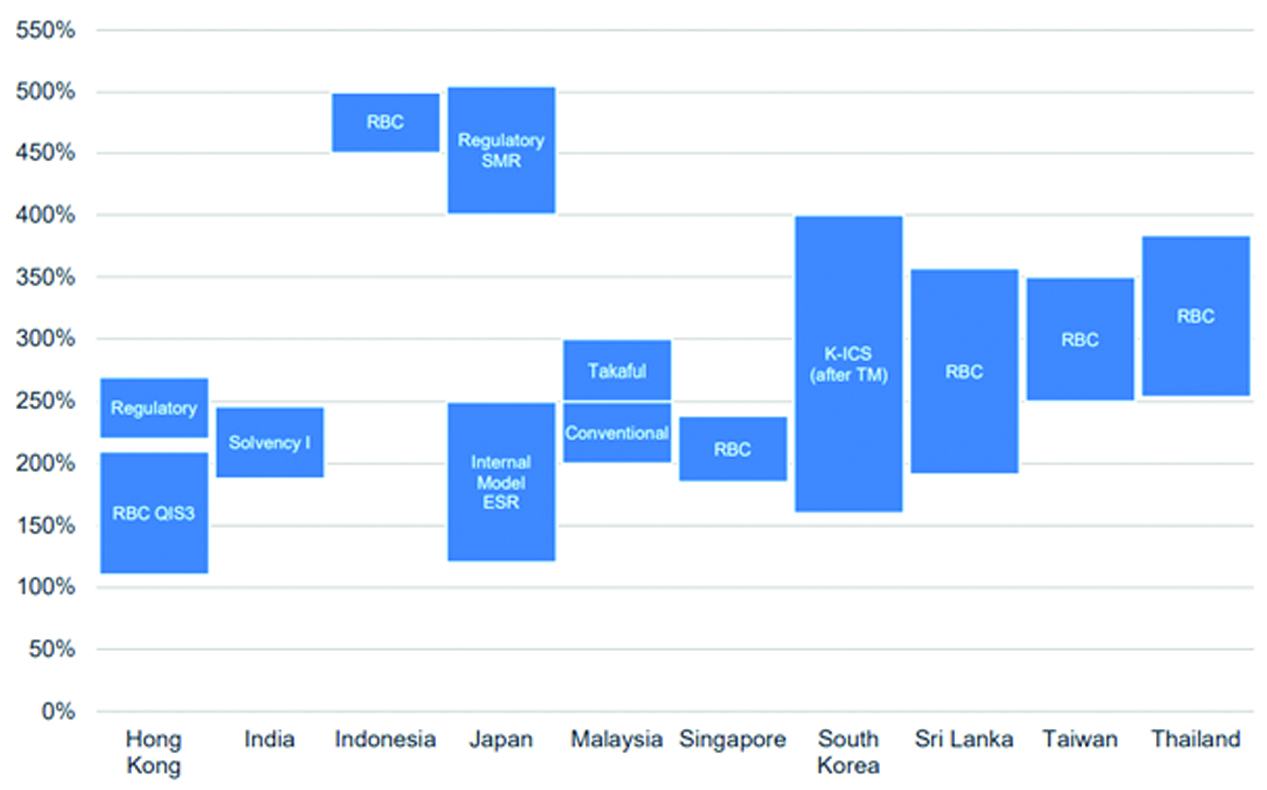

The RBC solvency ratio of companies across Asian countries is reflected below. It considers ratio of companies from higher band to lower band as compared to the industry standards.

Challenges and Preparedness Gaps

Despite its long-term benefits, implementing RBC in Nepal will not be without challenges mentioned below:

1. Data Limitations

- Many insurers don’t yet have deep, reliable datasets on claims experience, persistency, mortality, morbidity, or asset performance.

- Without granular historical data, capital charges may be based on approximations, which can distort true risk exposure.

2. Actuarial and Analytical Capacity

- RBC requires advanced actuarial modeling, stress testing, and scenario analysis. Nepal’s talent pool in these areas is still thin.

- Heavy reliance on a handful of actuaries or consultants can create bottlenecks and uneven implementation.

- Greater demand for risk management qualified personnel

3. Technology Infrastructure

- Many insurers still operate with legacy IT and siloed systems.

- RBC demands integrated platforms that can connect underwriting, investments, and risk management to produce timely solvency reports.

4. Awareness and Governance

- Boards and senior management need to fully grasp how RBC affects strategy, not just compliance.

- Embedding risk culture—so that business lines consider capital efficiency in pricing, product design, and investments—is still a work in progress.

5. Regulatory Transition

- Clear rules, templates, and timelines are still being shaped by the Nepal Insurance Authority.

- A phased or parallel-run approach is essential, but in practice this can create confusion and uneven preparedness across insurers.

- The capital charges for available asset class seem to be on higher side in the scenario of limited instruments available which is impacting the solvency of the insurer.

6. Market Structure and Capital Pressure

- Smaller insurers with limited capital buffers may struggle to meet new requirements.

- This could trigger pressure to raise fresh capital, merge, or exit certain high-risk product lines—shifting the competitive balance of the market.

7. External Environment

- Nepal’s broader financial system—limited capital markets, concentration of investment in fixed income securities and a few asset classes—restricts insurers’ ability to diversify risks, which RBC frameworks assume.

Addressing these gaps will require coordinated action by insurers, industry associations, regulators, and academic institutions.

Benefits to Policyholders and the Economy

Ultimately, the RBC regime is designed to serve policyholders, the insurance industry, and the broader economy. Key benefits includes:

1. Enhanced Policyholder Confidence

Knowing that insurers are adequately capitalized relative to their risk profiles builds trust in long-term commitments like retirement planning, children’s education policies, or annuities.

2. Lower Systemic Risk

By minimizing the probability of insurer failure, RBC contributes to financial stability and reduces the need for bailouts or regulatory rescues.

3. Responsible Product Innovation

Insurers will be incentivized to develop capital-efficient, customer-centric products that align business sustainability with policyholder needs.

4. More Resilient Investment Portfolios

Improved investment governance will ensure that insurers funds are managed prudently, benefiting not just policyholders but also national capital markets.

Strategic Roadmap for Nepal’s Insurance Sector

To make the most of the RBC transition, stakeholders must act in concert:

For Insurers:

- Invest in actuarial talent, IT systems, and ERM frameworks.

- Conduct dry runs and scenario analyses.

- Engage with boards to align business strategy with capital efficiency.

For Regulators:

- Adequate steps to ensure that insurers are facilitated with transitional challenges

- Facilitate industry dialogue and capacity-building workshops.

- Adopt a phased approach with impact assessments.

- Reassessment of capital charges for each assets class based on availability of instruments

For Industry Associations:

- Standardize practices and templates.

- Organize training for executives, boards, and middle managers.

- Serve as a bridge between regulatory intent and field-level execution.

Conclusion: From Risk Measurement to Market Maturity

Nepal’s adoption of a Risk-Based Capital regime is more than a regulatory upgrade — it is a litmus test for the maturity of the insurance industry. The fall in average solvency ratios from 295% to 228% shows that the old comfort was partly an illusion. What looked like strength was often just idle capital; what now looks lean may actually be capital working at its most efficient, but margin of error is small for such companies.

The challenge ahead is twofold: insurers clinging near the minimum must strengthen or risk regulatory intervention, while those with solvency well above 300% must stop hoarding safety and put their capital to work — through growth, dividends, or innovation.

RBC is not just a compliance hurdle. Done right, it is Nepal’s chance to align solvency with strategy, efficiency with resilience, and finally separate insurers that are merely surviving from those that are truly building for the future.

Authored By:

Amit Kumar Keyal , Deputy CEO, Nepal Life Insurance

About the Author:

Amit Kumar Keyal is the Deputy CEO of Nepal Life Insurance Company Ltd and a thought leader on insurance strategy, regulatory transformation, and inclusive finance in emerging markets.