Introduction: A familiar headline hiding uncomfortable details

India’s insurance sector has expanded in size, product variety, distribution footprint, and regulatory ambition. Yet, when the conversation returns to the two most widely tracked indicators of mass insurance adoption-insurance penetration (premium as % of GDP) and insurance density (premium per capita in USD)-the story remains stubbornly mixed. The IRDAI Annual Report 2024-25 data shows that India is not collapsing; it is stagnating at levels that are too low for an economy of our scale, especially when benchmarked against global averages.

The central message from the report is simple but significant: overall penetration is flat, and the non-life engine remains structurally weak, while life insurance has softened marginally. This is not a “cyclical” problem alone. It is a design and delivery problem-how insurance is packaged, priced, distributed, serviced, and trusted by households and enterprises.

1) What the report shows: Penetration is flat, life is slipping, non-life is stuck

Total penetration: steady at 3.7%

The report indicates that India’s total insurance penetration remained at 3.7% in 2024-25, unchanged from 2023-24.

At first glance, stability looks comforting. But penetration is meant to rise as incomes, assets, and formal finance grow. A flat number in a growing economy suggests that insurance is not becoming more embedded in the financial life of citizens and MSMEs.

Life insurance penetration: from 2.8% to 2.7%

The data shows life insurance penetration declined from 2.8% (2023-24) to 2.7% (2024-25). This decline matters because life insurance is still the largest contributor to overall penetration. Even a small drop in life quickly offsets incremental gains elsewhere.

What this may indicate (critical view):

- Protection is still not the default choice; savings-led and market-linked products dominate many buyer journeys.

- Persistency and long-term stickiness remain weaker than they should be-policies sold are not always policies sustained.

- Trust and value perception issues persist; consumers compare “return expectations” with other financial products and conclude insurance is “not worth it”, especially when suitability is unclear.

Non-life penetration: fixed at 1.0%

The report shows non-life penetration remains stuck at 1.0%.

This is arguably India’s biggest structural weakness. In most mature markets, non-life protection deepens steadily as households insure homes, liabilities, health riders, personal accident, cyber, travel, pets, and small businesses, alongside commercial lines.

In India, outside motor and a narrow slice of health and commercial insurance, many risks remain uninsured. A flat 1.0% signals that large sections of society still see non-life insurance as:

- Compulsory (motor), or

- Employer-driven (group health), or

- Claim-difficult (a perception problem), rather than

- A routine protection purchase.

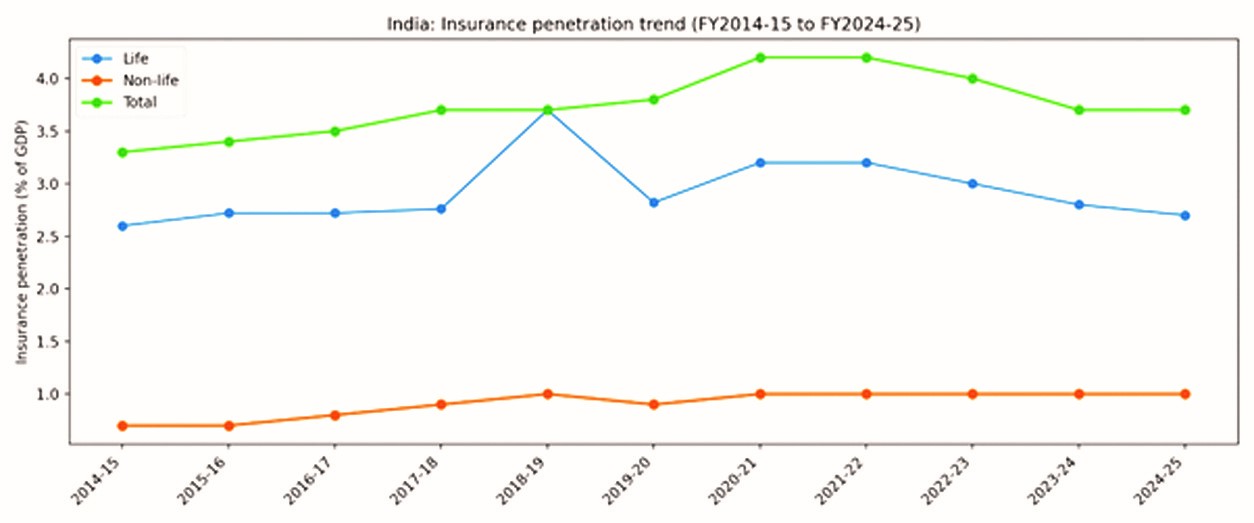

2) The longer trend: India peaked and then fell back

The report’s historical series (FY2014-15 to FY2024-25) shows that India’s total penetration climbed up to around 4.2% (FY2020-21 and FY2021-22) and then slipped back to 3.7% by FY2023-24, where it remains in FY2024-25.

This raises a key question: why did penetration not hold when the economy reopened and digitisation accelerated?

A critical explanation is that the pandemic years created a temporary spike in risk awareness and protection buying, but the system failed to convert that spike into a permanent behavioural shift. In practical terms, we may have:

- Acquired customers without retaining them,

- Sold policies without building deep trust in claims,

- Improved access without improving understanding, and

- Expanded product menus without making products simpler.

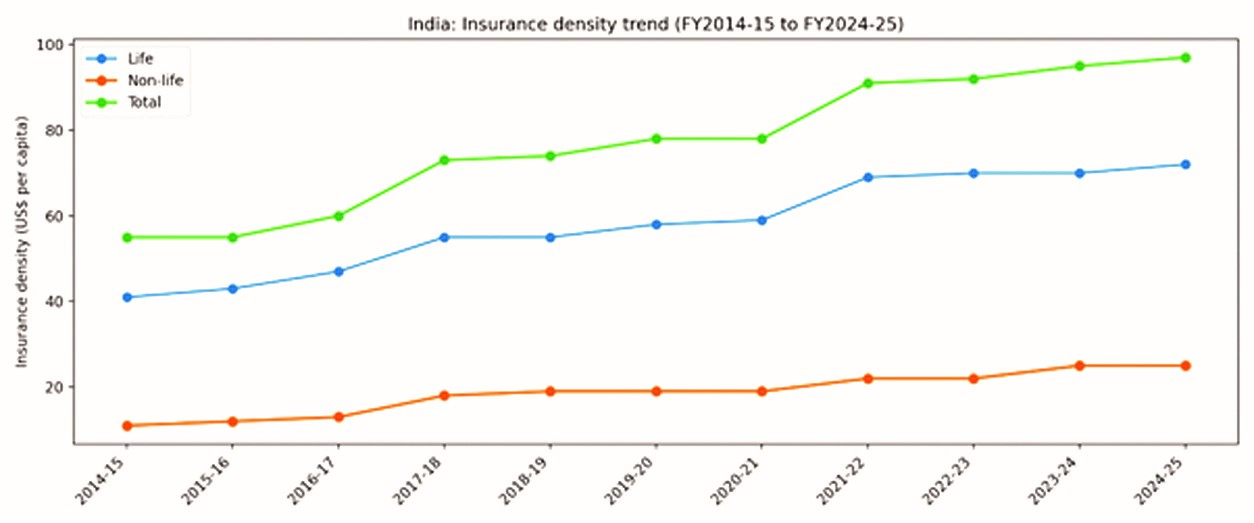

3) Density: improving slowly, but still far from where India should be

Total density: from USD 95 to USD 97

The report shows India’s total insurance density improved from USD 95 (2023-24) to USD 97 (2024-25).

Life density: up; non-life density: flat

Life density moved from USD 70 to USD 72, while non-life density stayed around USD 25.

What this implies:

India is spending slightly more per person on insurance, but the increase is modest and appears concentrated. When density rises but penetration stays flat, it often suggests that:

- Higher-ticket urban segments are paying more, while

- Mass-market participation is not expanding proportionately.

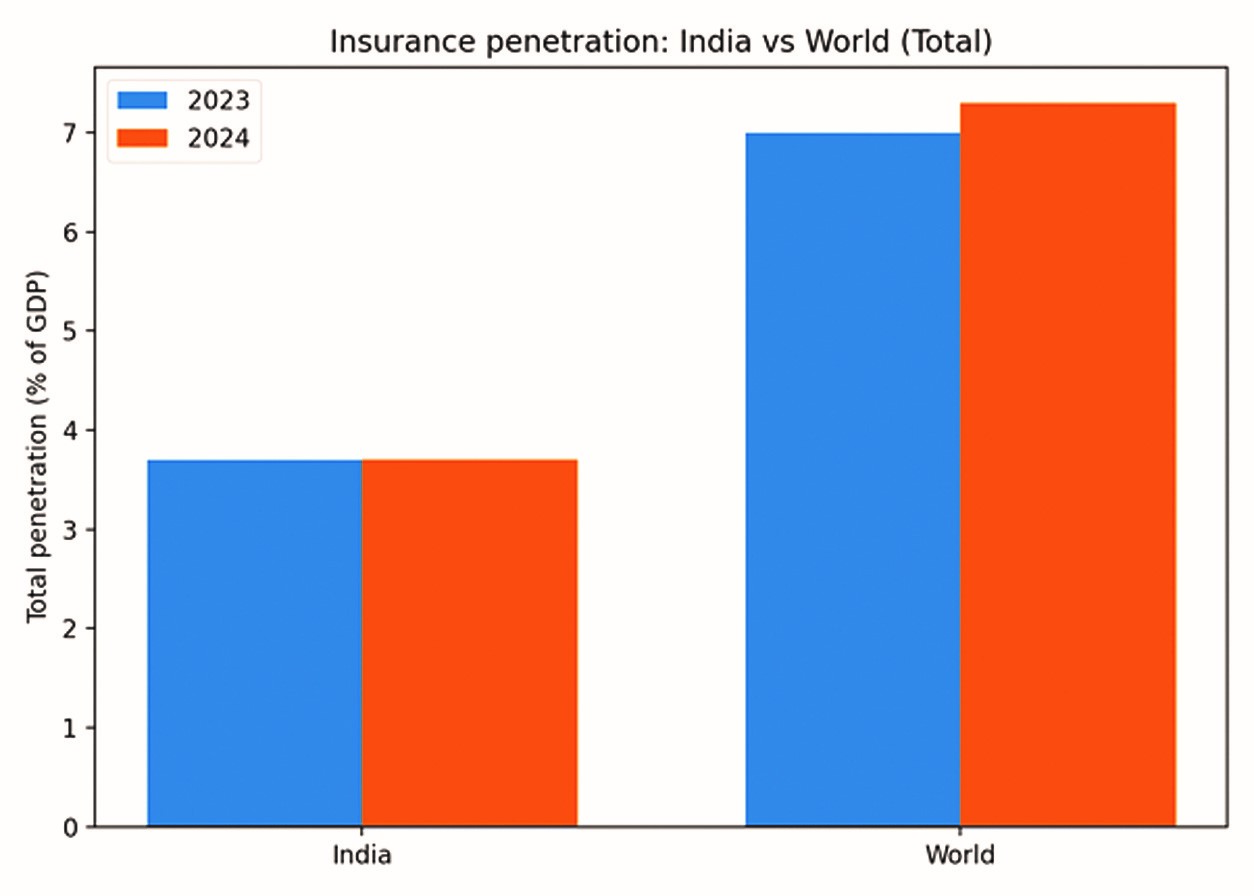

4) India vs world: The gap is not narrowing

The IRDAI report provides direct comparison with global averages.

Penetration comparison

- World total penetration: 7.3% (2024)

- India total penetration: 3.7% (2024-25)

India is roughly about half of the global level. The more serious story is within segments:

- World non-life penetration: 4.3% vs India 1.0%

This indicates India’s protection gap is not mainly a life insurance gap-it is a general insurance depth gap.

Density comparison

- World total density: USD 943 (2024)

- India total density: USD 97 (2024-25)

This means India is at roughly one-tenth of global per-capita insurance spending.

This means India is at roughly one-tenth of global per-capita insurance spending.

5) Where we are lacking: the real constraints behind the numbers

(A) Non-life has not become a household habit

For penetration to rise meaningfully, non-life must move beyond motor and narrow health coverage. India still lacks scale in:

- Home and contents insurance,

- Liability covers for individuals and small businesses,

- Personal accident as a default household cover,

- Small-ticket microinsurance that stays active,

- Catastrophe/climate risk solutions at mass scale.

Why this matters: a country can improve life insurance penetration through savings-linked buying, but true “protection culture” is built through non-life breadth.

(B) Life insurance is not converting awareness into sustained protection

The decline in life penetration suggests gaps in:

- Product suitability and clarity,

- Long-term persistency,

- Affordability of adequate sum assured,

- Distribution incentives that prioritise first-year sales over long-term policy health.

(C) Claims experience remains the strongest lever-yet under-used

Penetration is ultimately a trust metric. People buy and renew when:

- Claims are paid quickly and fairly,

- Documentation is minimised,

- Grievance resolution is predictable.

India’s market has improved, but perception lags reality in many pockets. The system still doesn’t consistently “market claims confidence” at the grassroots level.

(D) Distribution has expanded, but not enough “embedded rails” exist

Even with more channels, insurance is not yet seamlessly built into:

- Borrowing journeys,

- Msme payment ecosystems,

- Housing society ecosystems,

- E-commerce checkouts,

- Mobility subscriptions,

- Healthcare pathways.

Insurance remains “sold” more often than “activated” as a default protection layer.

6) What should have been done already (and why progress is slower than expected)

1) Standardised simple products should have scaled faster

India needed mass-adoptable, easy-to-understand products with:

- Standard benefits,

- Transparent exclusions,

- Plain-language wordings,

- Predictable claims processes.

Progress exists, but not at the scale required to move non-life beyond 1.0%.

2) Persistency-first regulation and incentives should have been stronger

A sustainable life market requires incentives linked to:

- Renewal quality,

- Long-term servicing,

- Suitability and disclosures,

- Lower lapses.

3) Insurance literacy needed local delivery, not just national campaigns

Insurance adoption grows when education happens at:

- Shgs, colleges, MSME clusters,

- Panchayat/municipal ecosystem touchpoints,

- Employer ecosystems, and

- Local influencers (agents as educators).

4) Claims visibility should have been treated as a national growth strategy

Public trust improves when credible claims stories become mainstream, regionally communicated, and measured.

7) The trust deficit in insurance

Despite regulatory reforms and market expansion, trust remains a key barrier to higher insurance penetration in India. Many customers continue to view insurance as complex and claims-uncertain, shaped by experiences of unclear policy wordings, mis-selling, exclusions discovered at claim stage, and inconsistent post-sale support. This results in policy lapses in life insurance and low voluntary uptake in non-life covers beyond mandatory products.

Bridging this trust deficit requires a shift from sales-led to experience-led growth. Clear communication, simpler products, predictable and faster claims settlement, transparent disclosure of claims performance, and stronger accountability of intermediaries are critical. Insurance penetration will rise sustainably only when customers trust that insurance will respond reliably when it is needed most.

8) What needs to be done now: A practical action agenda

I. Fix non-life penetration through “default protection”

- Push embedded insurance at scale (lending, housing, commerce, mobility).

- Expand MSME protection bundles (property + liability + business interruption).

- Drive personal accident as a default family cover (low premium, high impact).

- Build climate and catastrophe solutions using parametric models and public-private participation.

II. Make life insurance protection-led and long-term

- Move the sales narrative from “returns” to “income protection”.

- Improve persistency through better suitability, renewal nudges, and simplified servicing.

- Deepen annuities/pension solutions with clarity and confidence-building.

III. Treat claims experience as a growth KPI

- Publish claims servicing benchmarks in consumer language.

- Standardise and reduce documents where feasible.

- Improve grievance resolution turnaround with visible accountability.

IV. Rewire distribution incentives

- Reward long-term servicing and persistency.

- Upskill intermediaries with structured education (not just product training).

- Strengthen compliance to reduce mis-selling and protect trust.

Conclusion: Penetration won’t rise by capital alone-only by redesign

The IRDAI report’s penetration and density tables are a reality check. India is not short of intent, regulation, or innovation. But the data confirms that access and availability have not yet translated into mass adoption.

The next phase must focus on making insurance:

- Simpler to understand,

- Easier to buy and renew,

- Smoother to claim,

- And embedded into everyday life and enterprise decisions.

If India aims to close the protection gap meaningfully, the central battle is not just awareness-it is trust, product simplicity, claims experience, and non-life depth.