When will the war in West Asia end? For now, no one has a definitive answer.

Every war brings profound human suffering. Lives are lost, families displaced, cities damaged and economies destabilised. Supply chains fracture, diseases spread and inflation follows close behind. The conflict involving Iran, Israel and the United States is no exception. Yet its consequences are amplified by two structural realities.

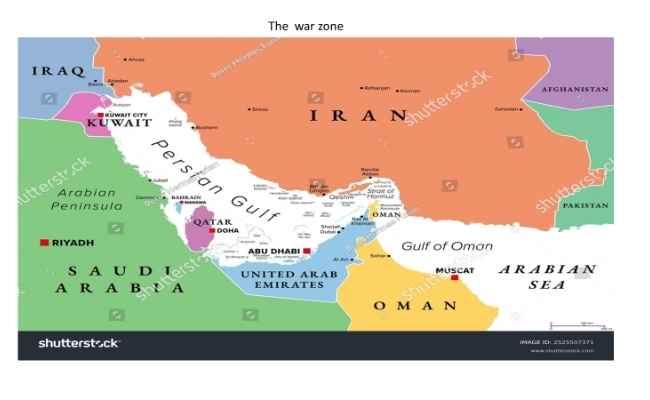

First, nearly one fifth of the world’s oil trade passes through this region. Second, the geography of West Asia places some of the world’s most critical maritime routes within proximity of potential conflict zones. Together, these factors make the region exceptionally sensitive to geopolitical shocks.

For exporters and importers, the consequences are already becoming visible. Cargo owners face daily reports of insurers withdrawing war risk cover at short notice or reinstating it only at sharply higher premiums. Shipping lines are limiting vessel availability. Freight rates are climbing. Voyage times are lengthening. In some cases, cargo is being discharged at intermediate ports, while contracts are cancelled altogether.

Against this backdrop, it is useful to examine how marine insurance responds to war risks and what exporters and importers can realistically do to limit financial exposure.

Direct vs Indirect Impact of War

The financial consequences of war for cargo owners fall into two broad categories: direct impacts and indirect impacts.

A direct impact occurs when cargo in transit suffers physical loss or damage due to a war-related peril. These risks are covered under marine cargo insurance when the Institute War Clauses (Cargo) are attached to the policy. It is precisely this war cover that insurers and reinsurers are currently cancelling or repricing in high-risk zones.

Indirect impacts are far more common but largely uninsured. These include higher freight costs, delays, disrupted supply chains, cancelled contracts or shrinking profit margins. Marine cargo insurance has never been designed to compensate for such commercial consequences.

Understanding this distinction is critical for exporters and importers attempting to assess their risk exposure.

Pre-Existing Risk Restrictions

Two important factors are often overlooked.

Indian cargo insurers have generally not provided automatic war cover for shipments to the Gulf region since 2022 because it has been classified as a High-Risk Area. Such coverage could still be obtained, but only through payment of an additional premium.

In addition, cargo movements to or from Iran have long been excluded due to sanctions provisions embedded in insurance policies.

What War Insurance Actually Covers

The Institute War Clauses (Cargo) define the specific circumstances in which insurers will compensate cargo owners. These include loss or damage caused by war, civil war, revolution, rebellion or hostile acts between belligerent powers. The clauses also cover capture, seizure or detention arising from such hostilities, as well as damage caused by derelict weapons of war such as mines, torpedoes or bombs.

However, a crucial limitation often escapes attention. The clauses explicitly exclude claims arising from the frustration of a voyage. In other words, if a ship cannot complete its intended journey because of war and cargo is discharged at an intermediate port, the financial consequences of that disruption are not covered.

The exclusion is clearly stated in the policy wording itself:

In no case shall this insurance cover 3.7 any claim based upon loss of or frustration of the voyage or adventure

This distinction becomes particularly important in the current environment, where shipping routes may change abruptly due to security concerns.

Three Situations Cargo Owners May Face

Exporters and importers trading with entities in conflict-affected regions typically face three operational scenarios.

The first arises when cargo is already on board a vessel that has sailed and is currently within the conflict zone. In such cases, cargo owners should remain in constant communication with the shipping line to understand operational decisions. They must also confirm whether war risk cover is in force. If the cover has been withdrawn, it is advisable to obtain war risk insurance immediately, even if the premium is significantly higher.

The second scenario involves cargo that has sailed but has not yet entered the conflict zone. Under these circumstances, reaching the original destination may no longer be possible. The vessel may choose to discharge cargo at a nearby safe port, return to the loading port and terminate the contract of carriage, or, in the case of full vessel loads, divert the cargo to an alternative destination if the cargo owner agrees.

Each of these options has important insurance implications. If cargo is discharged at an intermediate safe port, the shipping line will typically issue a notice terminating the contract of carriage. Once that happens, cargo insurance coverage also ends unless the insured promptly notifies the insurer and negotiates continuation of cover on revised terms and premiums. Importantly, war cover usually ceases because the intermediate port becomes the deemed final destination under the policy.

If the vessel returns cargo to the original load port and the contract of carriage is cancelled, similar insurance considerations apply. Coverage terminates unless insurers are notified and agree to extend protection. Beyond insurance, exporters may face complex commercial consequences such as reversing export benefits, finding alternative markets, absorbing storage costs or renegotiating freight arrangements. These are indirect consequences of war and are generally uninsurable.

A third possibility arises when cargo is diverted to an alternative destination. In this case as well, insurers must be informed so that coverage can continue under revised conditions. Freight charges may increase significantly, and cargo may need to be sold at distressed prices. Again, these are commercial losses rather than insurable ones.

When Cargo Has Not Yet Sailed

The final scenario involves cargo that remains at an Indian port awaiting shipment to a conflict zone.

Shipping lines may cancel the contract of carriage altogether. Even if they do not formally terminate the contract, the lack of vessels willing to sail into a war zone can effectively halt shipments.

Cargo owners must promptly notify insurers if they wish to continue insurance coverage during this period of uncertainty. Insurers will require clarity on how long the cargo will remain in storage and what the eventual shipping plan may be.

For perishable goods or commodities with limited shelf life, delays can create an additional complication. Even if the cargo policy remains active, deterioration caused by delay is excluded under the Institute Cargo Clauses, meaning such losses will not be recoverable.

A Realistic Approach to Risk

For exporters and importers, the most practical course of action is to assess their exposure carefully and maintain open communication with every participant in the supply chain, including shipping lines, brokers and insurers.

Cargo owners should never assume the scope of coverage under a marine insurance policy. Policy terms must be reviewed carefully, especially in times of geopolitical instability. Above all, it is important to recognise the limits of insurance. Marine cargo insurance with war clauses can protect against physical loss or damage arising from hostilities. It cannot, however, shield businesses from the wider economic disruption that conflicts of this scale inevitably produce. In moments like these, risk management depends as much on commercial agility as on insurance protection.

Authored by:

Balasundaram R, Head of Marine Insurance at Policybazaar for Business